Dr. Guna Raj Bhatta

1. Background

Nepal has made substantial progress in financial development over the years. Financial sector development took momentum after the mid-1980s and further expedited after the 2000s, resulting in better financial access, efficiency and deepening.

The financial liberalization process was initiated with the economic stabilization program of the International Monetary Fund (IMF) and the structural adjustment program of the World Bank in 1985. At that time, strengthening government banks, allowing private sectors in the banking business, opening up businesses for private and facilitating international trade were the major agendas of the reform (Ozaki, 2014). After the restoration of democracy in 1990, the post- democracy government remained liberal in the role of the private sector. That introduced additional private banks and financial institutions (BFIs).

During the early 2000s, the country launched a second-stage reform in the financial sector, of which some programs are still being continued. Financial liberalization programs were introduced in the presence, products, costs and returns of the banks. As a result, financial institutions and their branches surged rapidly, new financial products came into practice, and financial deepening indicators topped even neighboring countries.

Afterwards, financial consolidation measures, emphasis to access and literacy were in top priority. The payment system development, including the financial infrastructure, rapidly developed. This reform agenda is still being continued. However, Nepal’s financial sector has often been blamed for being unable to support the economic growth and employment, citing the poor growth performance, frequent asset price bubble and massive emigration for work and study abroad. In this background, I attempt to dig out one key issue of balancing between financial institutions and market development.

2. Role of Financial Sectors to Economic Development

A developed financial sector is presumed to be one of the major prerequisites for economic development. Empirical literature, including King and Levine (1993) and Levine and Zervos (1998) shows a positive relation between the developed financial sectors and economic growth. The general argument is that a better-developed financial sector promotes saving, enables the efficient allocation of financial resources and provides channels for sharing risks. In addition, a developed financial sector increases the productivity of economic growth.

The financial sector has also been perceived as an engine of sustainable economic development. It has positive implications for distributing the growth dividends (Balakrishnan et al., 2013). Likewise, a deepened and efficient financial system provides better ways of financing as well as an effective intermediation service. It further supports the proper allocation of risks and returns among stakeholders. A developed financial sector also helps lower both the risks and costs in producing goods and services, working as a lubricant for growth and employment (Sen, 2010). Similarly, an efficient financial system enables the environment for external finance, thereby addressing the financing constraints necessary for economic growth. Therefore, financial development is a prerequisite for promoting not only domestic investment but also attracting foreign investment.

Financial sector development has implications for the effectiveness of monetary policy transmission. Financial development comprises two factors, namely, financial institutions and markets. Financial institutions comprise banking, insurance, non-bank financial institutions and mutual funds, while financial markets comprise both stock and bond markets (Sahay et. al.., 2015). Balanced financial institutions and markets complement each other for mobilizing short- term and long-term financial resources. Both institutions and markets matter to mobilize sources of saving and sectors to invest, distribution of risk and returns, among others, being complimentary to each other. For example, a well-developed bond market facilitates the financing of large fiscal deficits domestically without inflationary pressure (Turner, 2002) and supports the effective implementation of monetary policy, making its instruments available (IMF, 2004). It is also realized that an inefficient capital market makes the financial system vulnerable in many ways. For instance, a poor market leads to an adverse selection and moral hazard problems for households in allocating savings, and it promotes certain family groups to invest as a substitute for the market (Herring and Chatusripitak, 2001). Therefore, the balance between financial institutions and markets is advocated for effective monetary policy transmissions.

3. Growth of Financial Institutions in Nepal

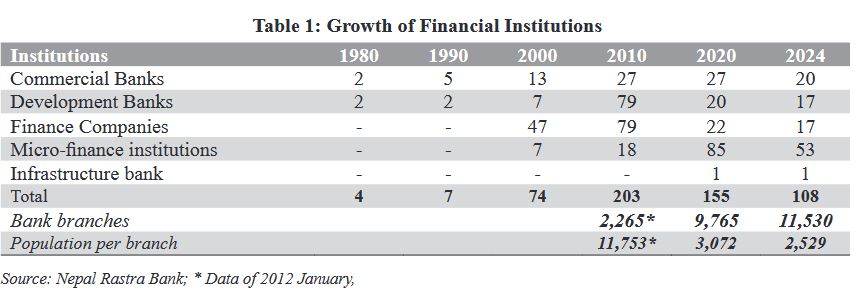

Nepal’s first bank was the Nepal Bank Limited, established in 1937 as the first commercial bank that functioned as financial intermediary. The momentum in the financial sector development came only after the establishment of Nepal Rastra Bank (NRB) as a central bank in 1956. There was a very limited number of banks and financial institutions (BFIs) in Nepal until the early 1980s. Until 1980, there were just four financial institutions licensed by the NRB, and all of them were fully government-owned. The growth in the number of financial institutions escalated after the introduction of a financial sector reform program in 1985 that induced the involvement of the private sector in financial services. The number of commercial banks, that were 3 in 1985, expanded access rapidly, reaching the total number of BFIs close to 300 in 2011 (Table 1).

Despite the significant growth in the number, effective and efficient intermediation is also questioned while some institutions started problematic and over-concentration to cities and the Kathmandu valley. In the meantime, financial consolidation measures were introduced in early 2011, with mergers and acquisitions, which are still in place. Even after the financial consolidation measures taken in the last decade, the financial services are expanding rapidly despite the reduction in size (Table 1). The financial sector liberalization and the reforms have significantly financially deepened the economy over the years. For instance, the broad money-to-GDP ratio was about 23 percent in 1980 and rose fivefold in 2024. Likewise, the credit-to-GDP ratio was 8 percent in 1980 and soared to 91 percent in 2024 (Table 2). This has put Nepal’s position to financial deepening far ahead in South Asia, being comparable to the level of advanced economies.

Despite the significant growth in the number, the effective and efficient intermediation is also questioned. In the meantime, the NRB introduced financial consolidation measures in 2010 with a moratorium on new licenses, mergers and acquisitions, and problem bank resolutions. It gained momentum in the later phases with a capital hike plan. These all substantially reduced the number: 164 banks and financial institutions merged to become just 42 in a short period, by December 2018, after the NRB’s policy of mergers and acquisitions. Up to July 2024, 301 BFIs were involved in mergers/acquisitions and have become 133 (Table 3). The financial consolidation measures have been perceived to be the most successful policy of the NRB in the region.

4. Status of Financial Development in South Asia and Nepal’s Position

The financial service indicators of selected economies at the financial deepening (money supply and credit flow), efficiency (interest rate spread) and access (bank branches) are compared. Table 4 presents the status of these indicators in 2023. Nepal’s financial service indicators are very much competitive with the neighbouring economies and at the top of the rank in some indicators. For instance, in 2023, Nepal had the highest financial deepening indicators: broad money to GDP ratio (120.8 percent) and private sector credit to GDP (91.7 percent) in the South Asian region (Table 4). Nepal stands at the topmost list in the Asian region as well, with a similar trend to the advanced economies. The other performance indicators, such as efficiency indicated by the interest rate spread, are also competitive, being third efficient in the region. The financial market indicators and the market capitalization ratio are also after India.

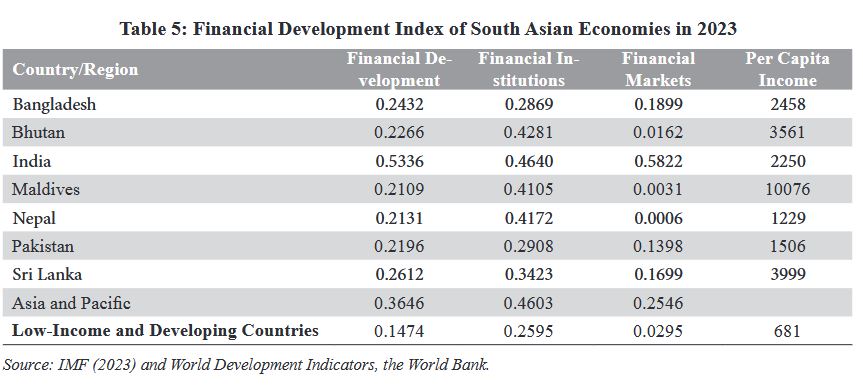

Following the methodology of Svirydzenka (2016) and developed by the IMF (2023), comparative data on the financial development situation in South Asian economies is presented in Table 5. The data covers both the money market and capital market instruments of the financial system: financial institutions and markets. In Table 5, financial development is considered both financial markets’ and financial institutions’ depth, access and efficiency. Financial institutions’ depth includes the ratio of private sector credit, non-bank financial institutions and insurance to GDP, while bank branches and ATMs serving populations measure the access. Institutions’ efficiency is measured by interest margin, spread rate, and returns, among others. On the other hand, the financial market’s depth is measured by the ratio of market capitalization, stock traded and debt securities to the GDP. Market access is the percentage of market capitalization out of the top 10 companies and the number of debt issuers. The financial market’s efficiency is measured by the stock market turnover ratio.

As per the Financial Development Index, Nepal’s financial market is at the ground level compared to financial institutions. The overall financial development index is similar to that of Pakistan and the Maldives and well above that of low-income and developing countries. The financial institutions index is much better, being higher than the average of low-income and developing countries. Nevertheless, the financial market index is the lowest in the region. This indicates that Nepal’s financial market development is the poorest in South Asia. The poor market development has substantially lowered the overall financial development index. Overall, most of the countries have better financial institutions, but very few of them have stronger financial markets. For instance, India has higher market development than institutions followed by Bangladesh.

5. The Key Issue

Despite Nepal’s success in expanding financial deepening and financial consolidation, the financial sector’s contribution to economic development has often been questioned. The financial development data of Table 5 provides Nepal’s key challenge of unbalanced financial institutions and market development, while previous tables provide overwhelming progress. While India has further developed financial markets than institutions, Bangladesh and Sri Lanka are following India.

Nepal has been the lowest performer in South Asia in the financial market. Nevertheless, Nepal places third position in terms of financial institutions, after India and Bhutan, being well above the low- income average and closer to the Asia-Pacific average. This indicates that a less-developed financial market has been substantially affecting the financial system in supporting productive investment, thereby employment and economic growth. The higher growth trajectory of India and Bangladesh in the region in the last decade also indicates this trend.

The argument of financial institutions’ role in the asset price bubble and little contribution to growth can also be looked at the way that financial markets not supporting institutions to channelize resources for the productive sector. Another argument could be the fact that financial institutions may be obliged to fulfill the financial market’s role, which may result in liquidity mismatch and poor market intermediation. Thus, we can argue that Nepal’s financial sector is still premature, with an unbalanced development compared to the world markets. Despite the phased reform programs, the overall development of the financial sector remains low, especially on the financial market front. An empirical research by this author under review identifies that financial markets do play a larger role than financial institutions in smothering business cycles. Furthermore, Nepal’s business and financial cycles do not synchronize with each other, while India’s do. These findings also evidence why Nepal’s financial development is not able to promote economic growth.

6. Conclusion and Way Forward

The general perception is that both financial institutions and markets should go in a coordinated way to have a developed financial system. When financial institutions lead, but the market is behind, long-term capital formation from the financial system will be affected. This broken channel may thus hamper the capital formation, thereby affecting employment and economic growth that Nepal has been experiencing. Nepal has the highest financial deepening indicators in the South Asian region. The need is to develop the financial market in all three dimensions of access, depth and efficiency. A balanced financial market and institution’s development is therefore a necessary condition to moderate the economic cycles, re-orient resources, and maintain macroeconomic stability.

[Dr Guna Raj Bhatta is Deputy Director at Nepal Rastra Bank]

7. References

Balakrishnan, R., C. Steinberg and M. Syed. 2013. “The Elusive Quest for Inclusive Growth.” IMF Working Paper No. 13/152. June.

Herring, R and N. Chatusripitak. 2001. “The Case of the Missing Market: the Bond Market and Why It matters for Financial Development”, Wharton Financial Institutions Center Working Paper, University of Pennsylvania.

IMF. 2004. “Monetary Policy Implementation at Different Stages of Market Development,” International Monetary Fund Board Paper.

IMF. 2018. Financial Development Index Database, International Monetary Fund: Washington DC. _____. 2023. Nepal: Third Review under the Extended Credit Facility Arrangement-Press Release; Staff Report; and Statement by the Executive Director for Nepal. International Monetary Fund: Washington DC.

King, R. G., and R. Levine. 1993. “Finance and Growth: Schumpeter Might be Right.” The Quarterly Journal of Economics 108(3):717– 37.

Levine, R., and S. Zervos. 1998. “Stock Markets, Banks, and Economic Growth.” The American Economic Review 88:537–58.