Binod Bajagain

Kathmandu, May 3: “Payment system” means a system for the payment, clearing or settlement of any type of payment claim or liability between service recipients, institutions or banks through any payment instrument (Payment and Settlement Act, 2019). The Payment and Settlement Act, 2019 lists the payment instruments (Section 31) to include Cash, Electronic Banking, Payment Cards, Interbank Payment, Mobile Banking, Electronic Wallets etc.

The definition and instruments list include all the contemporary payment services provided by Nepali Banks and Financial Institutions (BFIs) as well as Payment related institutions. The act also categorizes the payment related institutions into Payment System Operators (PSO) and Payment Service Providers (PSP), based on their area of service.

Digital Payment in Nepal

On the basis of size/purpose, payment systems could also be divided into retail and large value payment systems. Nepal Rastra Bank has been operating the Real Time Gross Settlement (RTGS) system since 2019 as the large value payment system. Whereas, the retail payment systems are operated by NRB licensed entities. Some of the major retail payment systems are NCHL’s connectIPS, FonePay Interbank Fund Transfer (IBFT), Mobile Banking, Mobile Wallets, QR Codes based payments (from mobile and web applications), eCommerce Payment platforms, Point of Sale (POS) devices etc (NRB, 2025).

Digital Payment Status in Nepal

Currently the digital payment usage ranges from Government payments and receipts to inward remittances. The person-to-government (P2G) payments e.g., tax/revenue payments, traffic fines etc. are integrated to retail channels (wallets, mobile banking). Almost all government-toperson (G2P) and government-to-business (G2B) payments are now routed through digital platforms. This includes salary payments through bank accounts, social securities in beneficiary bank/wallet accounts, vendor and parties’ payment in bank accounts through Electronic Fund Transfer (EFT) platform.

The capital market and public debt instruments are also dematerialized so that the payments and recording both are performed digitally. Recently, QR based cross-border payment acquiring (inward payments) has been started, whereas the cross-border payment issuance (outward payments) service from Nepal to India is still underway.

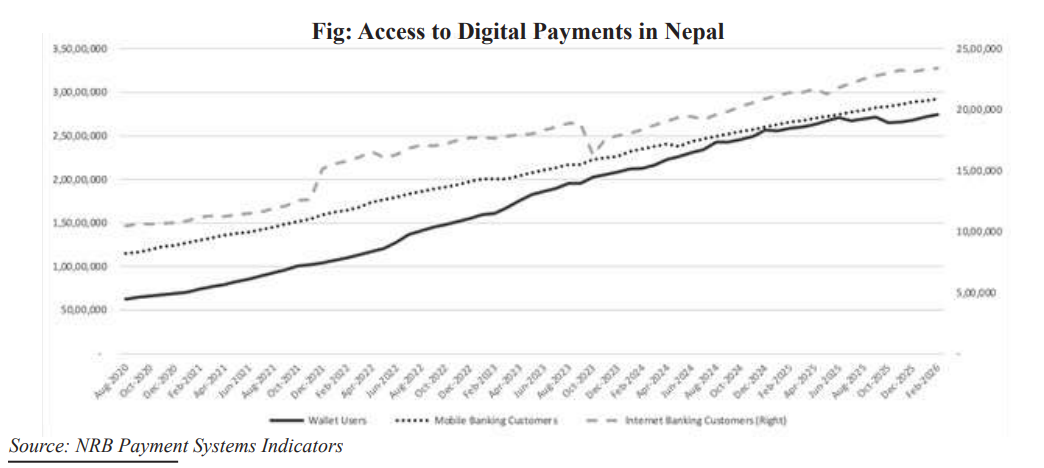

It can be observed that the number of wallet users quadrupled from 2020 Aug to 2025 July. In the same period the Mobile and Internet banking users have doubled. Such rapid adoption was primarily fuelled by the COVID pandemic, growth in internet and smartphone penetration as well as digital payment promotion strategies of the government.

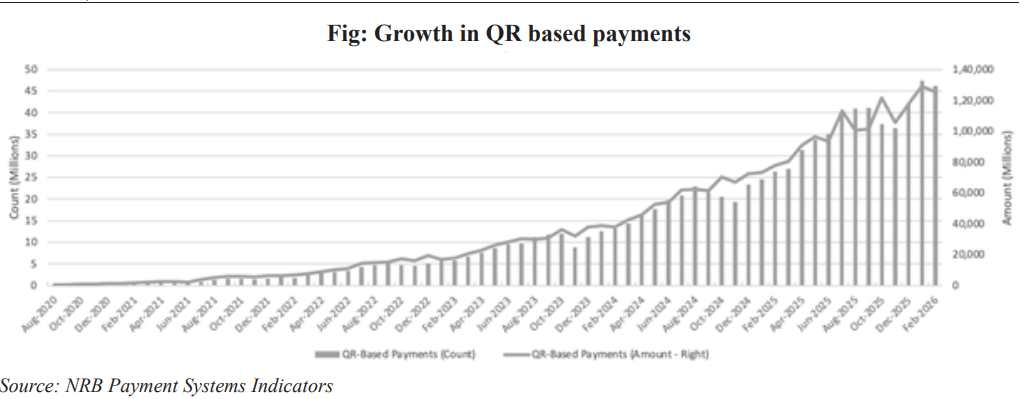

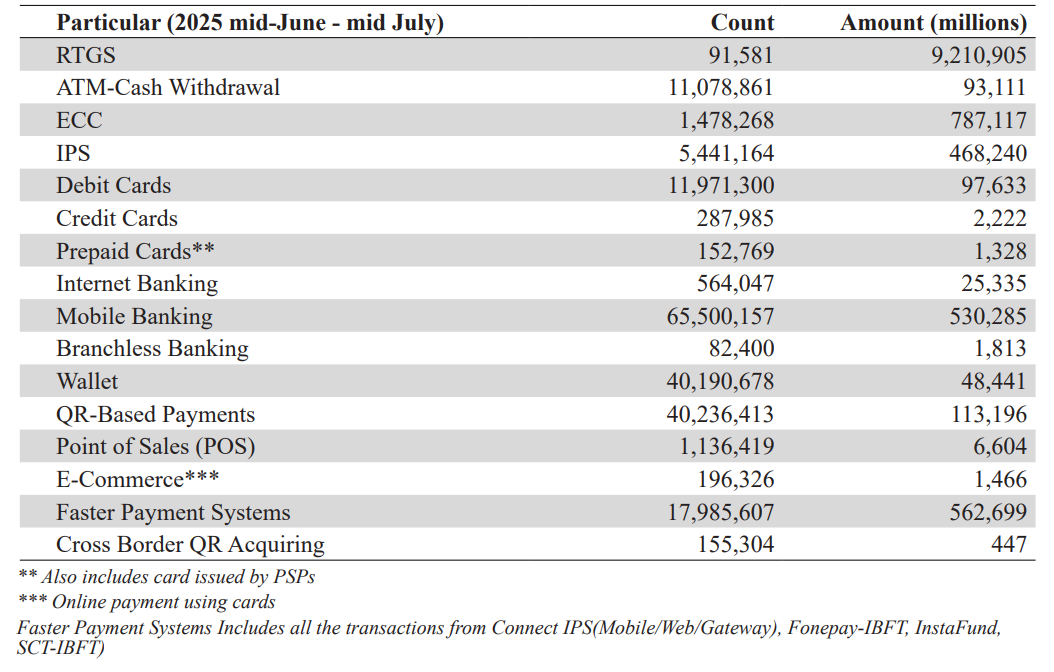

The growth of digital payment is also impressive. The rapid rise can be seen in both count and number of total transactions performed using various instruments. The usage of various digital payment for the period between mid-Jun 2025 to mid Jul is as follows:

Enablers for Digital Payment

The digital payment initiation started in the early 1990s by the introduction of payment cards and ATM machines in Nepal. This is gradually followed by other initiatives facilitated by rapid growth of the internet and mobile phones. There are various factors contributing to the wide reach and use.

1. Legal and Regulatory Initiatives

The payment or transfer via digital platforms and established private sector payment related institutions in Nepal started before the formation of separate legal framework. Nonetheless the current legal framework that followed the suite also contributed to expedite the growth in digital payments.

• The major legal and regulatory initiatives are:

• Nepal Rastra Bank Act, 2002

• Payment and Settlement Act, 2019

• Payment and Settlement Bylaw (First Amendment, 2023), 2020

• Payment System Inspection and Supervision Bylaw, 2021

• Nepal QR Standardization Framework and Guidelines, 2021

• Payment Systems Oversight Manual, 2021

• Digital Lending Guidelines, 2022

• Licensing Policy for Payment Related Institutions (First Amendment, 2024), 2023

• Payment Systems-Related Unified Directives, 2024

• Bank and Financial Digital Payment Related Onsite Inspection Manual, 2024

These initiatives formally empowered Nepal Rastra Bank to license, oversee and regulate payment systems of Nepal. Along with that separating the functions of different types of entities (BFIs, PSPs and PSOs) and their safety provisions as well as self-regulation mechanism boosted public confidence enabling increased adoption.

2. Institutional Initiatives

Growing number of Financial Service providers, branches of BFI’s and their customer base also enabled rapid growth of payment ecosystem.

Institutions that played vital role are:

• Bank and Financial Institutions (BFIs):

They integrate with PSP/PSOs to channel the fund load/unload on digital payment platforms. Also, banks offer mobile and internet banking platforms that provide faceless fund transfer facility.

• Payment System Operators (PSOs):

PSOs provide platform, software and infrastructure for interoperability and integration between multiple PSPs and BFIs. Moreover, they offer card schemes, settlement mechanism and link with merchants.

• Payment Service Providers (PSPs):

PSPs enrol customers, merchants and other parties and are responsible for providing payment interfaces.

• Telecom Operators (Telcos) and Internet Service Providers (ISPs):

By establishing nationwide cellular and broadband internet network Telcos and ISPs play key role in this payment evolution.

• Data Centre and Cloud Service Providers:

They provide cheaper data storage and host platforms for small to large enterprises.

. Software Solutions Service Providers:

They develop software solutions ranging from core (banking) systems to information systems to support customers and report the usage service provided.

3. Infrastructural Expansion

In last two decades there has been significant efforts for expanding digital payment related/ supporting infrastructures in Nepal. Some of the major infrastructural expansion contributing Nepal’s digital payment landscape are:

• National Payment Switch (NPS):

NRB and NCHL are in the final phase of fully commissioning NPS to integrate and streamline all the domestic payment transactions through common interface in the form of payment switch.

Some of the non-card scheme-based services of NPS are already rolled out. ConnectIPS is one of the widely adopted NPS product that acts as the backbone of Nepal’s interbank fund transfer service (Ahmed et al., 2025). After the full phased operation of NPS, the domestic payment channels will be interoperable as well as a separate card scheme for Nepal’s payment ecosystem will be introduced.

• National Payment Gateway (NPG):

To streamline its revenue collection and disbursement Government of Nepal took initiative through establishment of NPG. It contributed to the wide adoption of digital payment in government transactions. It’s estimated that more than 90% of government’s payment and more than 30% of revenue collection is now done digitally (Mulmi, 2023).

• National/Digital IDs initiative:

Although the distribution of National ID cards is snail paced, it is already integrated with Credit Information Bureau and other government services (Department of National ID and Civil Registration, 2025). After integrating National ID with telcos, NCHL etc. the customer enrolment and data sharing mechanism between financial institutions will become easier.

• Smartphone Adoption:

Smartphone is one of the major enablers because it’s essential for using most of the digital payment service. More than 73% of Households (2021 Census) are using smartphones that helped rapid penetration of internet and digital banking service in both urban and rural areas.

• Access to Broadband internet

In the last decade broadband internet penetration has also been rapidly. There are over 29 million broadband subscribers, with mobile broadband making up the majority at approximately 26 million users. Fixed broadband (e.g., fiber) now covers about 46.5% of households, while mobile broadband penetration has reached nearly 88% of the population. Additionally, there are over 39 million mobile connections, indicating a SIM penetration rate of about 132%, suggesting widespread multi-SIM use (NTA, 2026).

• Cheap QR Code

The introduction of costless QR Code/Stand setup motivated small and medium merchants to offer digital payment option. Before that merchants have to invest thousands of rupees in integrating PoS terminal and have to maintain constant connectivity to this network. As an offline payment alternative QR standee costs only a fraction than PoS terminal and need no internet connectivity.

Along with these initiatives, the reduced cost of cellular data (for e.g. USD 2.25 per gigabyte in 2019 to USD 0.46 per gigabyte in 2023) is also responsible for promoting rapid adoption of digital payment for outdoor use cases.

4. Promotional activities

Digital Nepal Framework (2019), Nepal Payment Systems Development Strategies (2014), Retail Payments Strategy (2019) are some of the major initiatives the government and NRB have taken to pave stones over the digital Nepal highway.

Moreover, some other initiatives that increased the digital payment adoption are:

• Campaigns for Financial Literacy and Digital literacy

• VAT refund on bill payment via digital channels

• Cashback on purchase through payment cards

• Jointly offering Financial Literacy and Digital literacy campaigns with private sector

The steep growth of (QR based) digital payments in early years of this decade also indicates COVID pandemic as an enabler of digital payment growth, as a contactless payment alternative to avoid contagion.

Barriers on Payment Systems Expansion

1. Infrastructural Limitations

The evidence from neighbouring and similar economies that surpassed Nepal’s digital payment growth seems to have various aspects more developed than that in Nepal. Lack of unified and well-designed infrastructure in Nepal has multiple impacts, ranging from the existence of less efficient redundant infrastructure and resources that fail to provide services efficiently.

a. Digital Public Infrastructure (DPI)

DPI is a set of digital infrastructure that can be shared among various entities and is mainly provided by the government (Centre for Digital Public Infrastructure, n.d.). This includes digital identity, payment platforms, data exchange protocols etc. that enables interoperable and scalable infrastructure. In the case of India, Aadhar System for digital identity, UPI for payments and India Stack for data exchange are some of the examples (Sánchez-Cacicedo, 2024).

b. Cloud Service

Cloud services are third-party-hosted infrastructure, platforms, or software that are accessible to users over the internet. These services allow for the flow of user data between client devices and the provider’s systems, enabling the development of cloud-native applications and flexible remote work (Red Hat, 2022). The existence of large cloud service providers viz. Amazon, Microsoft, Oracle, Google etc. in a country will provide cheap and secure infrastructure for hosting digital service.

Regulators are not allowing entities to host their system on foreign cloud platforms concerning data-localization compliance. This necessitates payment service providers to set up their own servers which is relatively costly and less flexible than cloud platforms.

c. Digital (National) Identification

Collecting Know You Customer (KYC) and personal details is the first step in every digital payment enrolment. National ID document viz. Citizenship, Permanent Account Number (PAN), Voter ID, Driving License among others are some of the widely accepted forms of ID proof. The paper printed forms of IDs lack digital means of verification. Thus, without digitization the traditional means of identification are not directly useful in payment system promotion.

The Government of Nepal introduced (Digital) National ID project in 2018. Initially planned to complete the enrolment and distribution throughout the nation within 5 years, the current adoption rate is snail paced. In this almost 8-year period, enrolment has been done for only 18 million people whereas less than 3 million cards have been distributed (Department of National ID and Civil Registration, 2025).

Lack of documentation and legally recognized identity is a significant obstacle in enrolling to financial services, verifying identity online, sharing information across payment platforms, and establishing credit scoring (Appaya & Varghese, 2019).

d. Reliability of Broadband (Internet) Connectivity

Nepal has seen significant growth in internet and mobile connectivity in recent years. But the reliability of the internet connectivity is quite low. This is mainly due to frequent power cuts, physical breaks and natural disasters. The challenging geographical terrains of Nepal is also responsible for poor connectivity quality. A reliable and dedicated internet/cellular connectivity is essential for growing digital payment in Nepal.

2. Low Digital Literacy and Awareness

The overall literacy rate of Nepal (2021 census) is 76.2%, whereas surveys have estimated the financial literacy rate of 57.9 and the digital literacy rate to be only 31% (Nepal Rastra Bank, 2022). People of old aged population or ethic group are still outside the radar due to language barriers. As most of the payment platforms are in English language and using new terminologies which is not familiar to people lagging formal education. Also, people are hesitant to open bank account, deposit their savings to banks and believe non-physical (digital) form of money.

3. Legal/Policy Gaps

Despite availability of basic legal framework, Nepal still lacks robust mechanism to enable data sharing, protection of consumer data and mechanism of honouring credit scores in financial sector. Although vouched for reducing risks, the tight daily and monthly transaction caps prevent customer from initiating high value payment via handheld devices. The clear legal frameworks including risk sharing, dispute redressal provisions in digital lending laws are necessary to promote rapid growth of digital lending, crowd funding and P2P lending platforms in Nepal.

4. Higher transaction fees

While some economies subsidize or even waive the merchant discount rate (MDR) for receiving payments, some merchants in Nepal are hesitant to accept payment digitally citing the high MDR. In India P2P fund transfer via UPI platforms is free but there is NPR 2-10 fee charged per transaction for interbank fund transfers in Nepal (IFC, 2025).

The fees for card-based payment, even due to international routing of payment instruction is relatively higher (2%-3%) in Nepal than other economies.

5. Reliability of Payment System

Adoption of digital payments in rural and less literate population of Nepal is also hindered by a “trust deficit” rooted in technical instability and rising security concerns. Frequent system downtimes, delayed transaction settlements discourage users from transitioning away from cash. This “trust deficit” is most evident in the continued preference for cash-on-delivery in e-commerce, where consumers opt for physical money-in-hand to avoid the perceived risks of digital unreliability and security breaches.

6. Settlement Timing and Practicability

To reduce the system burden and cost of interbank fund transfers, PSPs are settling merchant payments by batch processing. As some merchants prefer real-time receipt of money in their accounts, such time-gaped payment discourage them to accept digital payments. Moreover, while processing large ticket size, such time-gap might hinder merchants’ fund/liquidity management thereby requesting customer to use immediate crediting alternatives.

7. Cyber Security, Scam, fraud

Despite the rapid growth of QR-based systems, many small and medium enterprises (SMEs) remain reluctant to move away from cash due to rampant phishing, impersonation scams, and social engineering attacks.

According to Nepal Police Cyber Bureau data, financial scams and fraud cases nearly doubled in just one year, jumping from 4,112 in FY 2023/24 to 7,723 cases in FY 2024/25 accounting for over 40% of all reported cybercrimes. On average there are 52 cybercrimes reported per day in Nepal (Ray, 2025). Merchants are particularly wary of “accidental transfer” scams and the lack of robust, real-time grievance redressal mechanisms, which often leave them bearing the financial loss of fraudulent transactions.

Besides those, the traditional workflow in government entities, company and tax administration offices, and regulators are also barring startups in promoting modern payment instruments. There are increasing cyber enabled financial fraud and thus seeks immediate remedial of the issues.

Conclusions

While our progress regarding adoption of digital payment is remarkably appreciated, there is room for improvement to address issues of many unenrolled sectors and rural market. Rising number of grievances and sluggish redressable mechanism is further creating dissatisfactions among regular customers.

We should establish mechanisms for information and threat intelligence sharing to maintain awareness of existing and emerging risks and to leverage expertise of partners in areas where there are inadequate internal skill sets. The national ID, credit scoring, digital KYC and data sharing mechanism among operators will be next ice break in our payment ecosystem. #Nepal

[Mr Binod Bajagain is the Deputy Director at Nepal Rastra Bank. This article was adapted from Nepal Rastra Bank, Annual Journal, 2026)